Even with recent increased demand, many U.S. investors have limited experience using structured notes in client portfolios. With more education, added transparency and the right tools, more financial professionals can get comfortable using this flexible, risk-based investment.

Structured notes are popular in Europe and Asia, and although lesser known in the U.S., they are growing in popularity.

Because of their flexibility, payout structure, and defined risk characteristics, structured notes may be a compelling choice for investors’ portfolios.

Nevertheless, structured notes do come under fire and have been misunderstood in the U.S. for many years.

Unlike in the U.S., structured notes are almost exclusively a retail product in Europe and Asia. They became popular in Europe in the 1970s and really caught on in Switzerland, the United Kingdom and Germany. However, they are still relatively new in the U.S.

First coming across the pond in the mid-90s and utilized more throughout the early 2000s, structured notes have not been as accessible to investors in the U.S. as they have been in Europe.

Investment minimums of up to $1 million have made them inaccessible to anyone other than the ultra-wealthy, private banks, or institutional investors.

Because they are a relatively recent emergence and often inaccessible, many U.S. investors, even financial professionals, have limited experience using structured notes in client portfolios.

With limited access, relative lack of transparency and high investment minimums come misconceptions that could turn off U.S. investors from utilizing structured notes more—and understandably so.

At Halo we believe that with more education, added transparency and the right tools, more investors can get comfortable using this flexible, risk-based investment.

We’re going to take a look at a few common misconceptions of structured notes and in most cases, we hope to ease these misunderstandings with discussion of how structured notes are actually issued and designed.

1. Its A Very Risky Investment

Let’s start with the most common myth: structured notes are too risky.

Like any investment out there, there are different types of structured notes with varying degrees of risks.

Some structured notes can be risky (take a structured note tied to a startup biotech with no approved drugs, for example), while others have a risk profile more similar to that of bonds, with features including principal protection.

Certain structured notes are designed to be riskier investments, because they are oriented to have a higher potential payoff. However, most structured notes are designed to be risk-based because they offer two things—a measure of downside protection and some rate of return or participation.

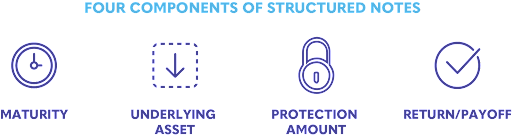

Generally, the majority of structured notes traded (whether they are built for income or growth) track the price return of a stock(s) or index. Although structured notes are tied to an underlying asset, they also have three other components that investors can adjust for their given investment situation.

The thing about structured notes is, they usually come with built-in downside protection.

So, unlike owning a stock outright, there tends to be some level of protective cushion with structured notes. This partial protection is based on the downward movement of the underlying stock or index.

In other words, investors may tend to think that structured notes are risky because of a lack of familiarity. Structured notes can provide a risk-managed middle ground between stocks and bonds when a level of protection is built into the investment.

2. Difficult to Understand & Extremely Complex

The next misconception we often hear is that structured notes are too difficult and complicated to understand. For the most part, this situation can be rectified with deeper understanding and education.

Most standard income and growth notes are composed of a zero-coupon bond, and an options package to generate the payout or return structure.

For example, let’s look at a standard growth/participation note that is based on the performance of a commonly-followed stock index. A note like this consists of a zero coupon bond (for the principal component) and typically some combination of options packaged together (for the growth and protection components).

The beauty of structured notes is that an investor doesn’t have to manage each of these components individually.

Of course, there are certain notes that may exhibit more complicated payouts, but those are less common compared to the notes that are most frequently issued and used by investors.

An income note is slightly more complicated as it consists of a strip of regular coupon payments with a series of short-term call options.

The tradeoff for an investor is whether they would be willing to overlay an options strategy with multiple expirations and strike dates on multiple underlyings in their portfolio. If not, then structured notes may provide one package that provides roughly the same payoff and/or return without managing each component separately.

Before investing with structured notes, the first task is to understand portfolio objectives. From there, a structured note can be used for either capital protection, yield enhancement or upside participation.

Learning how a bond works and adding an options overlay are the building blocks of starting to understand how a vast majority of structured notes function.

3. Its Structured Note Issuers vs. Investors

Finally, one of the most common misconceptions out there is that banks are betting against those who purchase structured notes.

While banks do initially take the other side of a structured note trade they will in many cases immediately hedge their risk.

Generally speaking, banks aren’t in the business of taking big positional bets on the markets, rather they prefer to be in the safer business of collecting fees.

Banks do get paid an upfront fee to create and issue structured notes, that’s part of the transaction cost. And that’s where banks want to make their money.

Since most structured notes tend to be long the stock market, if banks didn’t hedge their risk, they would all collectively be short the stock market ” definitely not something they want to do on a regular basis (if ever).

As such, banks will hedge their risk, often in exchange traded markets (like vanilla options) for their book of structured notes. They may have an overarching position from all their note issuances which they trade as one unified portfolio.

Individually though, each note they issue is hedged. In fact as odd as it sounds, many issuers are not averse to these investments performing well so investors continue to utilize them in the future.

Remember, the majority of a structured note is a zero coupon bond. For banks this is a relatively cheap form of debt funding they can secure versus issuing a corporate bond that may have all-in interest costs that are higher.

Structured note issuers want to issue cheap debt, earn a reasonable fee for creating the customized investment, and see the client happy with the result.

In other words, it’s very plausible that both the issuing bank and the note buyer makes money on the trade. Ideally that’s the way a healthy market should work.

Tradeoffs to Using Structured Notes

As with any investment, there are tradeoffs to using a particular vehicle in portfolios and education is one of the most important considerations.

There is the credit risk of the issuer, since notes are an unsecured debt obligation from banks. Although they are legally obliged to make payments on structured notes as promised, that promise is only as good as the financial health of the issuing institution.

Market risk, particularly with structured notes linked to equity underlyings, always carry the possibility that investors can lose some, or all, of the principal.

Liquidity is also a consideration for investors using structured notes. Since there isn’t a fully functioning secondary market for notes yet, investors should be prepared to hold a structured note to its maturity date, or risk selling the note at a discount to its initial value.

Some structured notes have call provisions that allow the issuer, at its discretion, to redeem the note before it matures at par value. If the issuer “calls” the structured note, investors may not be able to reinvest their money at the same rate of return provided by the structured note that the issuer redeemed.

When researching any investment, researching and understanding the investment vehicle is important for a positive experience. Halo makes education easier with a full suite of content to get more familiar with structured notes.

Changing Perceptions

As can be seen, some of the most common misconceptions of structured notes can be explained with education.

As is common with structured notes, investors can incur losses if sold prior to the date of maturity, or if the structured note is called by the issuer. This is another important consideration when evaluating structured note features.

Understanding the maturity, underlying, return and protection levels are key variables that every investor should know before investing with structured notes.

Learning the basics of how a note is created, issued, and held is generally a good starting point to having a reasonable familiarity with these popular and flexible risk-managed products.

Reach out to Halo for any other questions you may have on structured notes and other defined outcome investing products!

Securities offered through Halo Securities LLC, a SEC Registered Broker/Dealer and FINRA/SIPC member. Halo Securities LLC is affiliated with Halo Investing; Halo Investing is not a broker dealer. Halo Securities LLC acts solely as distributor/selling agent and is not the issuer or guarantor of any structured note products.

.jpg)